There’s money in property, and that’s good enough for Hong Kong

- Officials talk of diversifying the economy, but our tycoons, many of whom made their fortune in real estate, are admired for their success and indispensable to the government for their contribution to its coffers. Talk will remain just talk

I’ve little doubt what the typical Hongkonger would do if he or she won a lottery jackpot. Firstly, they would be secretive about who they tell for fear of having to unnecessarily part with cash. A portion would probably go to charity, but the biggest chunk would go into buying property – a large flat for the lucky winner, the rest for lifelong rental income. It’s an idea that flies in the face of good financial investment advice, which stresses the importance of diversification to limit risk.

The logic is that there is no better investment than property, which will usually go up in value and if down, only momentarily before resuming the march upwards. Americans and now Australians can relate otherwise and, of course, there is Hong Kong’s own economic downturns during the outbreak of severe acute respiratory syndrome in 2003 and the Asian economic crisis of 1998 to also prove otherwise.

But memories are short and anyway, the government, for all its talk of the future lying in innovation and technology, is firmly wedded to the same thinking.

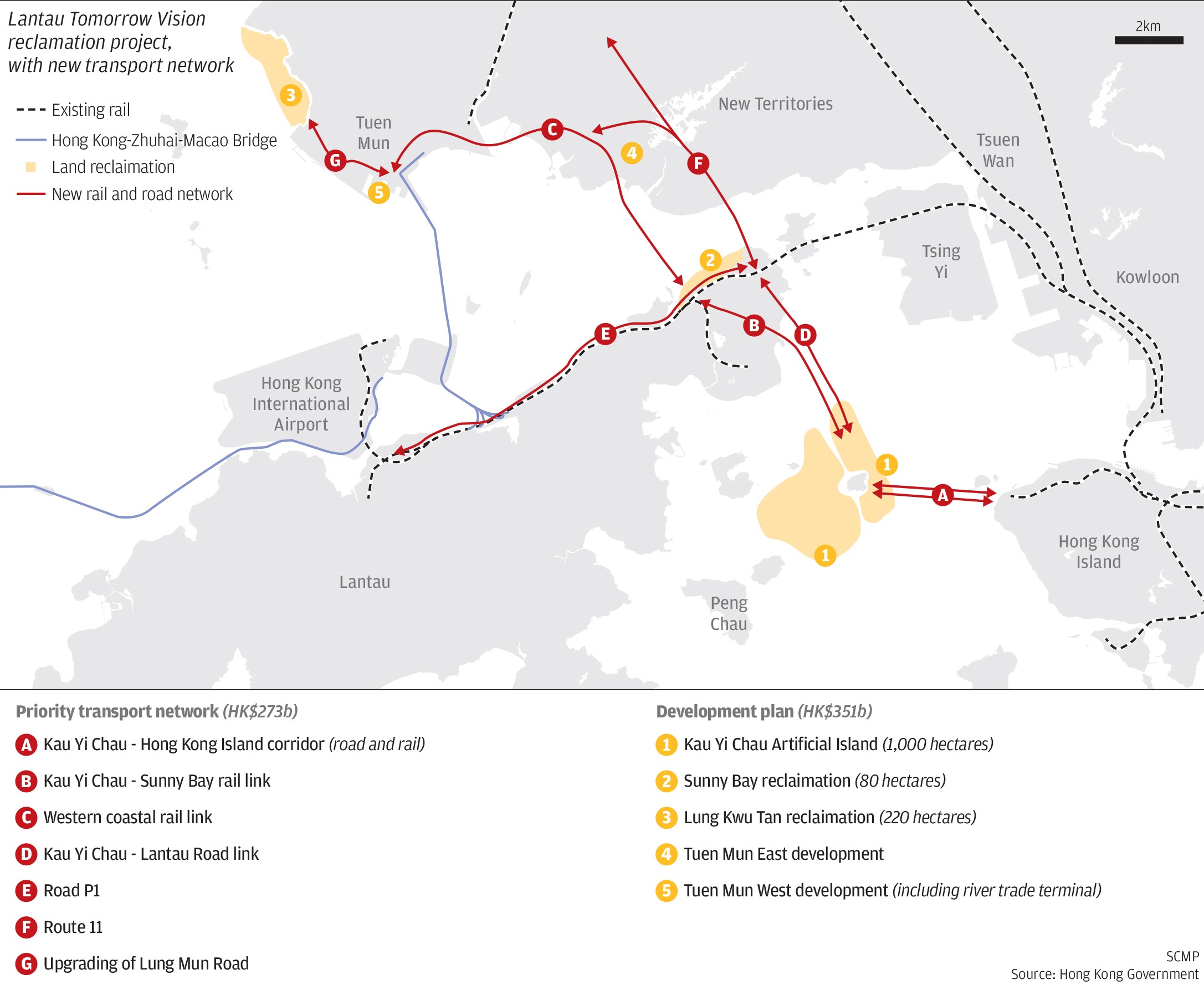

Land and its use is, after all, where the bulk of government revenue comes from, as has been the case since the British colonial government hit on the idea of reclamation to create extra revenue in the latter half of the 19th century.

Hong Kong stands out against other cities when it comes to such lack of diversity. While great rival Singapore has real estate magnate brothers Robert and Philip Ng of Far East Organisation at the top of the Forbes list for the city state, just eight of the top 20 make the majority of their income from property. There is a wide mix of ventures, from investment in a Japanese paint firm and an innovative hotpot restaurant chain to electronics and pharmaceuticals.

Billionaires behind oyster sauce, casinos, hotels and power companies also feature on Hong Kong’s rich list. But it is the property and real estate tycoons – Li Ka-shing, Lee Shau-kee, Joseph Lau, Kwong Siu-hing and Peter Woo uppermost among them – that Hongkongers most admire. They are also significantly wealthier than their Singapore counterparts, proving the money-grubbing potential of Hong Kong property – and perhaps making any such comparison unfair.

Ironically, these tycoons, so looked up to, are the same people who have helped make life so difficult and even unaffordable for Hongkongers, with rents cutting deep into incomes and ensuring that buying a home remains far out of reach for the majority.

For the government, addicted to revenue from land and taxes from property, it is also the reason Hong Kong will struggle to move into a new phase of development. You’ve got to wonder what all that talk about the city needing to look to the future and innovate means when the people in charge of making decisions are incapable of change themselves.

Peter Kammerer is a senior writer at the Post