Reign of US equities is here to stay, whatever the market chatter

Nicholas Spiro says momentum of the ‘America first’ surge may have slowed but US stocks remain the best bet for investors, given the persistent strains in Europe and emerging markets

Signs that the period of American leadership in equity markets may be nearing its end have been one of the most talked-about themes in investment research reports over the past several weeks.

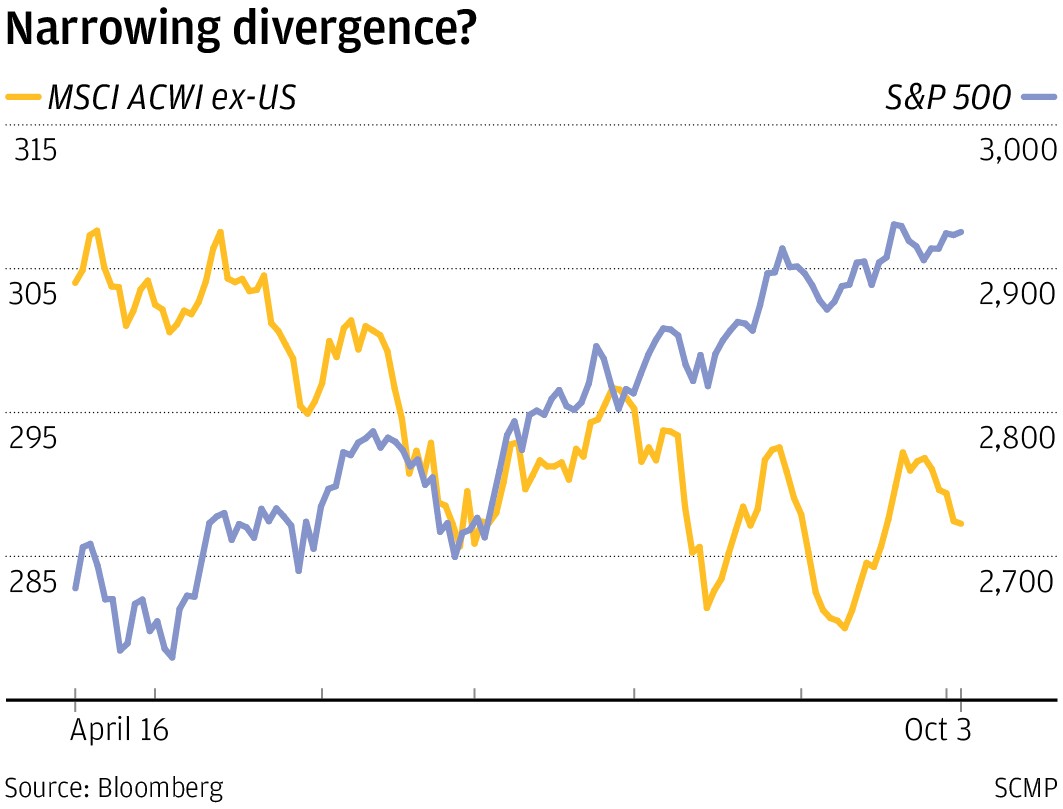

The divergence between US equities and those in the rest of the world has widened sharply this year. Since early May, the benchmark S&P 500 index has surged more than 11 per cent while the MSCI All Country World Index ex-US, a gauge of stocks in advanced and emerging economies which excludes American shares, is down nearly 3 per cent.

The contrast is even starker in the case of the most important equity markets in developed and developing economies. While the Russell 2000, a leading index of small companies that derive their revenues mainly from within the US, is up 8 per cent since early May, the Dax, Germany’s main equity index, and the Shanghai Composite, its Chinese equivalent, are down 4 per cent and 9 per cent respectively.

But over the past month, the divergence has begun to narrow. Not only has the S&P 500 only marginally outperformed the MSCI ACWI ex-US, the gap between America’s benchmark index and emerging market shares has diminished significantly, helped by a 3.7 per cent rise in the Shanghai Composite.

Speculation that the “America first” trade is beginning to unravel is being fuelled by a confluence of factors. These include the recent decline in the US dollar, a widening valuation gap that creates an attractive entry point for emerging market and European shares, and increasing concerns about the sustainability of the nine-year-long US bull market, which at the end of August became the longest ever.

Yet while American leadership in equity markets may not be as secure as it was during the summer, its successor has yet to emerge.

Some large fund managers believe the recent stabilisation of asset prices in emerging markets is laying the groundwork for a durable rally in 2019. There are certainly signs that sentiment has improved. A recovery in commodity markets since mid-September is providing a fillip to many developing economies, the leading producers and consumers of raw materials.

Watch: US reaches trade deal with Mexico and Canada

Other fund managers point to Europe as an alternative to pricey US stocks, partly because of this year’s sharp decline in the euro – the more than 7 per cent fall versus the dollar since mid-April benefits the region’s exporters – and the start of an interest-rate-hiking cycle in the euro zone next year, which should help the bloc's banking stocks.

However, renewed concerns about Italy’s commitment to the euro – amplified by the expected end of quantitative easing in the bloc in December – make euro-zone shares a risky bet.

This is why the case for convergence within global equity markets is unconvincing. As DataTrek Research, a US consultancy, rightly observed in a note published on Monday, “while non-US equities may look cheap on a valuation basis, investors have been cautious in trying to pick a bottom in either [Europe] or emerging markets”.

What is more, US equities continue to benefit from the prominent role played by America’s technology giants in powering the rally, in stark contrast to Europe, where the tech sector is almost non-existent in stock markets.

Investors should therefore stick with American stocks for the time being, while looking for pockets of value in emerging markets and the euro zone, particularly in developing economies with strong fundamentals and in European countries whose banking sectors are well capitalised and have exposure to emerging markets, such as Spain’s.

When it comes to global equities, America is likely to remain top dog for some time yet.

Nicholas Spiro is a partner at Lauressa Advisory