Higher interest rates loom as Federal Reserve faces the music on inflation

- If the Fed succumbs to pressure to act quickly on curbing inflation, higher interest rates will emerge in the US and cascade across the globe

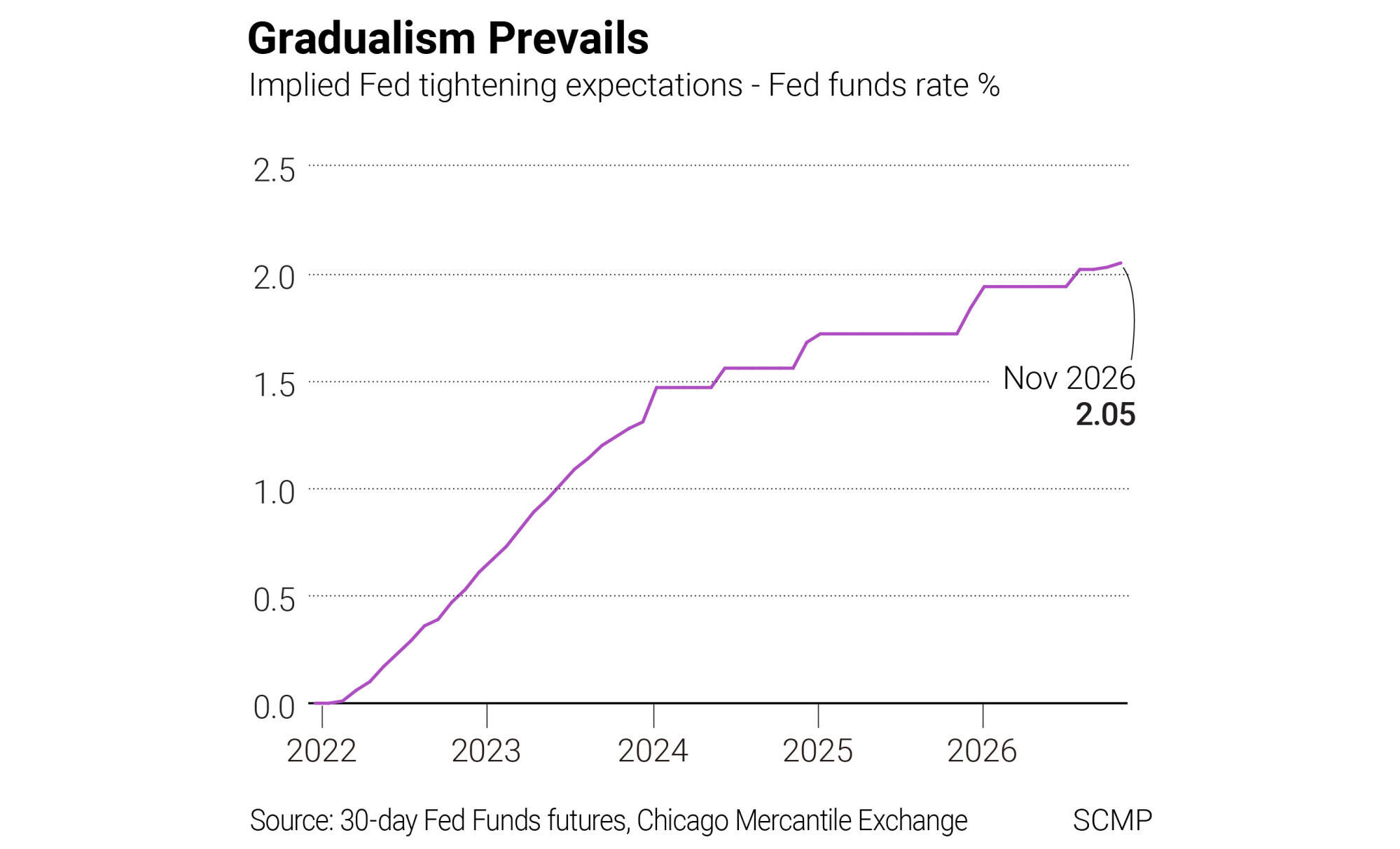

- Even if gradualism wins the day, though, the days of easy money and low interest rates are almost certainly coming to an end

Who’s afraid of inflation? Certainly not global equity markets, judging by the boom conditions rippling through the major exchanges right now.

The multitrillion-dollar question is whether the Fed is on the brink of removing the market’s “punch bowl” of cheap money, which was spawned by years of quantitative easing and debt buy-backs following the 2008 financial crash and has accelerated through the Covid-19 pandemic.

If the Fed is on the verge of hitting the panic button over inflation, then high noon looms for global interest rates. Once the United States sets the ball rolling for higher rates, it will pose deep challenges for China and frustrate any chance of easing monetary policy again in this cycle.

02:47

As Hongkongers struggle with rising inflation, the city’s most vulnerable are the hardest hit

There has never been a better time for calm nerves on the US Federal Open Market Committee (FOMC) when it meets this week to consider its policy options for the coming months. Its much-awaited interest rate decision is expected on Thursday.

One thing is clear. The “perpetual put” of low US interest rates put in place by former Fed chairman Ben Bernanke in 2008, when the global economy was close to collapse, has finally come to an end.

Right now, the market’s rate tightening expectations are not too fraught, but a lot depends on how much the Fed is prepared to rock the boat to bring inflation back into line. At the moment, the spread between the two-year US Treasury bond yield and the effective Fed Funds rate is factoring in around half a point of interest rate tightening over the next two years.

It is all down to what the Fed deems appropriate levels of interest rates to run the economy over the short, medium and longer term. At this year’s September FOMC meeting, the Fed Funds rate was envisaged to be heading towards a median rate of 2.5 per cent beyond 2024.

Under normal circumstances, interest rates should be targeting a return to 3 to 4 per cent for better monetary traction, but clearly not while the outlook for output, inflation and employment looks so uncertain.

Inflation, politics leave Powell’s Fed between a rock and a hard place

For the time being, there is a good chance the Fed will give the economy the benefit of the doubt, at least until the Omicron threat is more fully understood.

Whether Fed gradualism prevails or shock tactics take over, the world is on a one-way ticket to higher rates in the next few years. Beijing might be trying to pivot monetary policy towards a softer bias to reboot China’s domestic demand, but it will be swimming against the tide.

The global bias is towards higher interest rates. China will eventually have to follow suit.

David Brown is the chief executive of New View Economics