US dollar vs yuan: why China’s threat against HSBC rings hollow – for now

- The bank is accused of colluding with the US to take down Huawei, fuelling speculation it could lose its business in mainland China

- But with China’s efforts to internationalise the renminbi stalling, Beijing still needs HSBC to provide international access

What becomes of the Hong Kong dollar? Singapore may hold the secret

THE MIGHTY DOLLAR

The US dollar has had no serious contender for the role of global reserve currency: i.e., the pricing and trading mechanism for essential commodities and the fallback currency for developing nations.

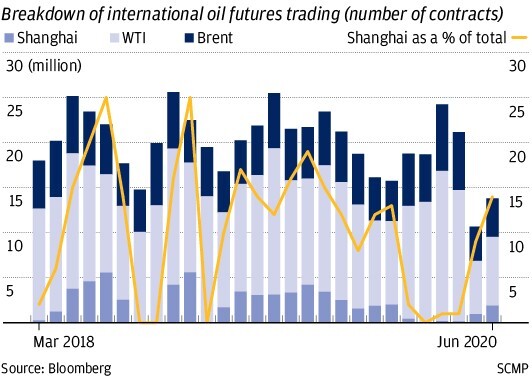

The mainstay of the dollar’s dominance in the global economy has been the fact that the two most important global commodities, oil and gold, trade in US dollars. As China has become the biggest importer of oil – with about 10 per cent of global consumption – and one of the largest buyers of gold, it made sense for policymakers to make an aggressive push to internationalise the renminbi and thus reduce the country’s reliance on the greenback.

A major step towards internationalisation of the renminbi was taken in 2018 when the Shanghai International Energy Exchange started to offer crude oil futures contracts priced in renminbi, successfully attracting traders from around the world and taking volume away from the two most popular contracts traded elsewhere: Brent and WTI. This move made a lot of sense, given that although a third of the world’s oil is consumed in Asia, it’s primarily traded elsewhere. However, the trade has seen intermittent spikes in volume, and has yet to demonstrate long-term popularity. Still, it has been much more successful than oil traded in yen on the Tokyo Commodity Exchange.

China urged to develop its own international payment system

DOLLARS ON THE STREET

The US controls the clearing of dollars in New York, allowing it to constantly track the movement of dollars. The exception is of course cash on the street, as big banknotes from all issuers have a habit of disappearing. This control is a powerful tool for keeping the world’s banks in check. Should the US deny dollar clearing to any bank that has fallen out of favour, it would make bank operations under the current global financial system very difficult and thus a good reason not to try and circumvent US laws.

02:30

Why Hong Kong pegs its currency to the US dollar

INTERNATIONALISATION? NOT MUCH PROGRESS

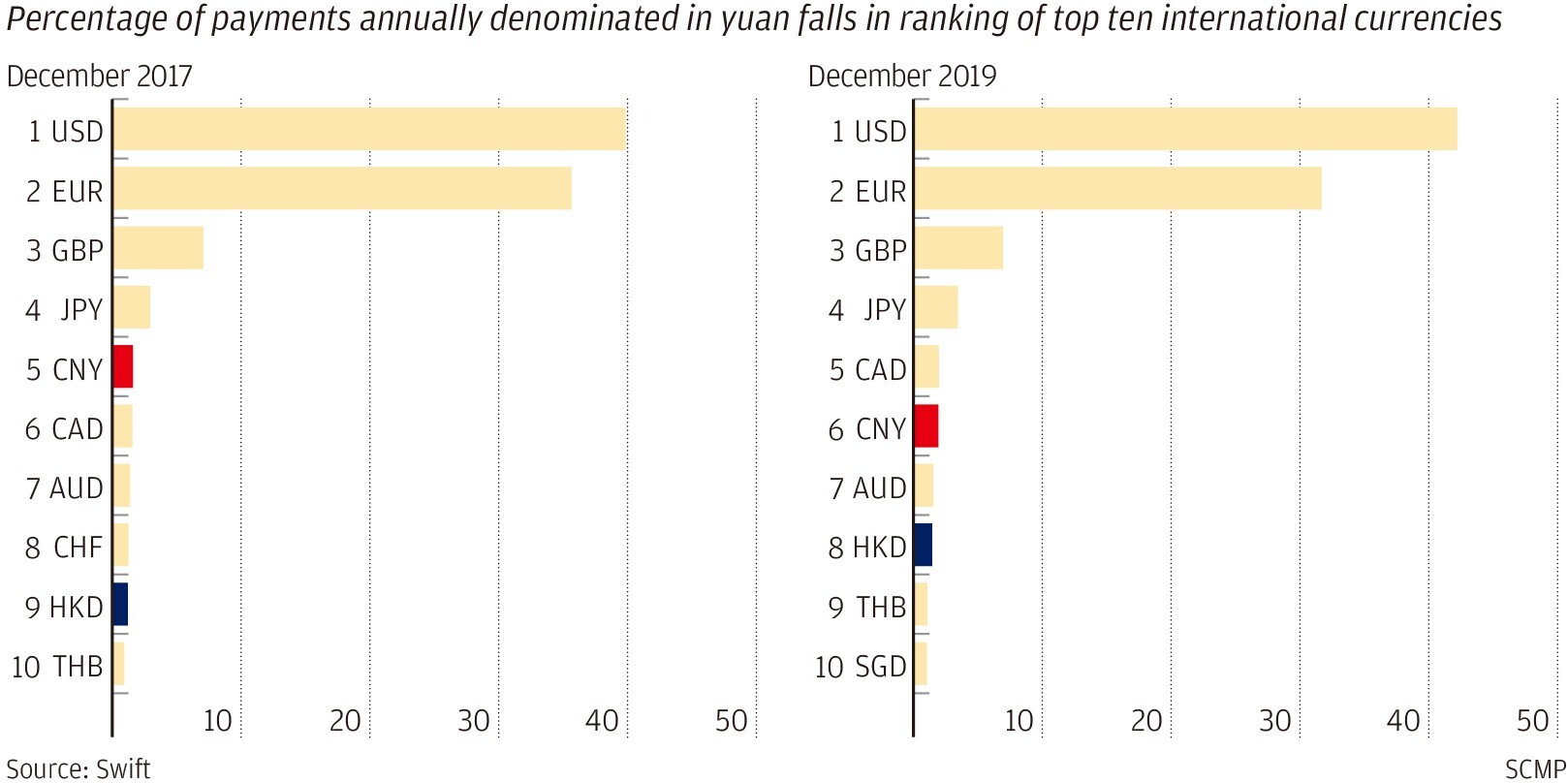

Each year, global financial transaction messaging system Swift announces the rankings of different currencies used in international transactions, a good indication of how the Chinese are doing in gaining international acceptance for the renminbi. Since its inclusion in the IMF basket of Special Drawing Rights (SDR) in Q3 2016, the international appeal of the renminbi appears to have diminished – contrary to expectations. At the end of 2017, it ranked 5th; in 2019, it ranked 6th, behind the loonie (CAD) and ahead of the Australian dollar. Most notably, the Hong Kong dollar moved up a position to 8th.

Losing a spot while little brother catches up is quite a blow for Asia’s largest economy and the world’s biggest exporter.

If China truly wants a global currency, that would mean scrapping exchange controls, a move that would be far too risky at the moment. Which brings me to HSBC’s issues.

US dollar payment system debate continues, can America cut China off from SWIFT?

HSBC IN THE CROSS-FIRE

HSBC is the piggy bank in the middle of a spat between Beijing and Washington which has now descended into accusations of spying, more arrests and forced closures of consulates. This showdown has now bled into the world of banking and could signify the start of a financial cold war, which will likely further pressure stock prices in the sector – including that of HSBC, which is already nearly 60 per cent lower than at the beginning of 2018.

There were suggestions during the week that HSBC could lose its China business as a result of the accusations – denied – that it colluded with the US government against Huawei. If that were to happen, another 10 per cent would easily come off the share price.

HSBC IS SHRINKING

Some 10 years ago, HSBC employed about the same number of people as the population of Iceland. Today it is about 23 per cent lower, at 257,000, and that is after the staff cuts announced earlier this year of 35,000. It seems the bank is on a path to restructuring, with reports that its chairman, Mark Tucker, is considering shuttering businesses in the US and EU.

HSBC employs about 8,000 staff in China, a drop in the bucket when compared to the global total, and nearly all of them were recruited locally. Yet, its reach is deep and very valuable, with 170 branches in 50 cities, making it the largest geographical network of any foreign bank in the mainland. This is what will save HSBC in the current firestorm.

Huawei to double down on HSBC as legal battle over extradition of Meng intensifies

When doing big business globally, there are only a handful of banks you can turn to for finance and HSBC is the most firmly entrenched in commercial lending to Chinese businesses. For that reason, and the fact that China is struggling to get the renminbi widely accepted, I think this frenzy remains a storm in a media teacup and HSBC will be able to brave it out in Asia – at least for now.

For HSBC shares, the rule of thumb for Hongkongers used to be buy below HK$60, safe as houses, and you can give them to your grandchildren. However, at HK$35 what do you do? If you loved it at HK$60, you should really love it at HK$35, right? In my view, investors should wait and focus on new restructuring plans from HQ in London before calling their broker. ■

Neil Newman is a thematic portfolio strategist focused on pan-Asian equity markets